Supermicro's Path to Mania

The Story Behind the Recent S&P Entrant

**This is a story/article I initially posted on X in March. I did not update for the recent earnings report, but the story is much the same. I hope you enjoy this deep dive!**

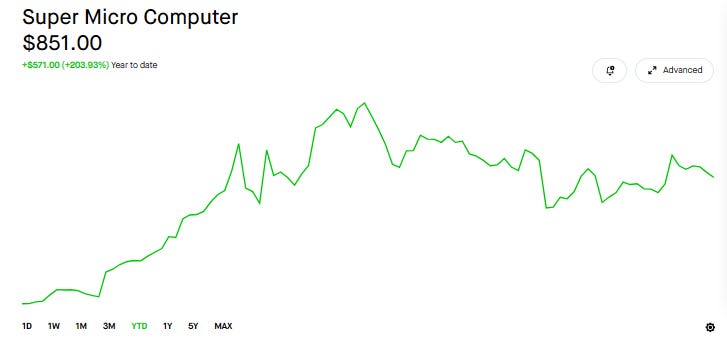

Supermicro Computer (SMCI) has been the subject of intense mania in 2024 with the stock up over 200% YTD.

Many investors are now left wondering: what is this company? How did they get here?

This story involves a rocket ship journey to prominence, an accounting scandal, and an uncontrollable geopolitical nightmare.

Let’s take a deep dive into Supermicro’s history.

It's been quite a wild ride.

The Founding

Charles Liang was born in 1956 and raised in Taiwan. He grew up near a forest where, according to him, he developed a deep love of nature. He would go on to be among the first graduates of the National Taiwan University of Science & Technology, or NTUST for short. He studied Electrical Engineering and is now named among the notable alumni.

Liang would then come to America to earn his Master of Science in Electrical Engineering from University of Texas at Arlington in 1987. After graduating with his MS, he would move out to San Jose, California.

San Jose, and all of Silicon Valley, was seen as the land of opportunity for someone with Liang’s education and prowess. The budding semiconductor industry would enable the Internet to eat the world. With the Internet, the world developed its insatiable hunger for computing power. Silicon Valley would become the hand that feeds this hunger, delivering innovation and breathtaking new technologies at dizzying speed. Underpinning all of this though, is hardware. Boring old servers cabled together in the complex networks that make up modern data centers.

Liang first spent several years as an engineer at Silicon Valley firms like Chips & Technologies and Suntek and would later become the President and Chief Design Engineer of Micro Center Computer in 1991. He held this position until the 1993 founding of Supermicro Computer.

Much like other Silicon Valley startup stories, Liang and his wife Sara co-founded Supermicro out of a garage. Charles would focus on the nitty gritty engineering while Sara managed the finances. The team grew from 3 to 5 and started out as a motherboard OEM. They would design motherboards and sell them to server OEMs.

By 1993, 30% of North American systems used Supermicro Pentium Pro motherboards, according to the company. In 1996, they opened a Taiwan subsidiary for high volume production and to meet voracious Asia Pacific demand for computer hardware. The company, Ablecom, would be led by Liang’s brother. They remain a critical vendor for Supermicro chassis to this day, and his brother is still the president. In 1998, they opened a subsidiary in the Netherlands to meet European demand for hardware.

Liang had one goal: to make higher quality products with better performance and to do whatever possible to reduce energy consumption. Moore’s Law made this easy, the tireless scaling of semiconductors would yield generation after generation of increasingly efficient chips. The same size chip would host twice as many transistors as the previous generation, so the compute capacity scaled much quicker than power usage. This holds true today, even though next-gen chips use more power, they offer substantially more performance.

Liang knew early on that staying on the leading edge would turbocharge growth. Customers want the best technology, so being first to market would enable Supermicro to win customers from incumbents like HPE and DELL.

He would later build this into the company’s mission: to always be first to market with new innovations. He wanted Supermicro products to always be better and faster.

In 2004, the strategy changed a bit. Liang took his kids out to see the movie “The Day After Tomorrow” and was struck by the prospect of environmental catastrophe. Tying back to his childhood love of nature, he added one final element to Supermicro’s strategy: Greener.

Better. Faster. Greener.

Liang built the organization from a dusty garage into a formidable hardware manufacturer by hiring people whose personal mission and vision matched the company’s. They were energized by the “Greener” vision, but Liang also made sure to pay his employees well. Supermicro has consistently paid above-average salaries, and since the IPO has offered all employees stock options. The family-centric foundation of the company would continue for years, a culture they have since outgrown.

Liang remains a very hands-on leader and still views himself as an engineer first. He holds numerous patents and keeps his product design roots close to heart.

The Better. Faster. Greener. strategy was a winning one. The company grew rapidly, tempering the dot com bubble and continuing rapid revenue growth up until the 2007 IPO.

The homegrown culture of Supermicro would lead to numerous issues though. In 2006, SMCI was fined $150k for violating the Iran embargo. They were selling hardware that they knew would end up in Iran and indicated as such in the settlement. They knew of this as early as 2004 and began cleaning up operational controls. But this was just the beginning of their troubles.

Going Public

On March 8th, 2007, the company would IPO and raise $64m, selling 8m shares at $8/share. By 2008 the company had 850 employees, but Liang would still obsessively check over every custom order. Customization was the company’s specialty, and he didn’t want to sacrifice their reputation for growth. Workdays could extend well into the evening, with employees working upwards of 15 hours.

The intense workplace environment still had a family-feel to it, though. On Saturdays, Charles and Sara would host lunches for employees that elected to work on weekends. Charles regularly worked 7 days a week. This culture began reaping benefits. According to the New York Times, more often than not the company would beat rivals to market by 3 to 6 months with the newest technology. They were rapidly growing too, and their approach evolved alongside this growth. They expanded from a simple motherboard provider to building entire servers and storage solutions from the ground up.

Their servers were always characterized by the company’s motto:

Better. Faster. Greener.

And this showed in customer wins. By 2009, they had 1,100 employees and growth was driven by major customer wins. They were popular with cutting-edge software providers like Elemental Technologies (who would go on to be acquired by Amazon, who needed custom hardware for their high-powered video compression software.

They also were a key partner for Apple's early data center buildout. META was also a key customer, as was INTC. In 2012, their 2U and 4U Tower “Hyperspeed” Servers would become popular among high-frequency trading firms, giving them inroads into the US financial industry.

In 2016 they shipped 30,000 Microblade Servers, most likely to Intel, with a PUE (Power Usage Effectiveness) of 1.06. A “perfect” machine would have a PUE of 1.00, and 1.06 was among the best performing systems available.

By 2016, Supermicro seemed to be in the perfect position. They were making inroads across the financial industry, their hardware was used by the American government, and they were a critical partner in the massive data center buildouts by Intel, Apple, and Facebook. Their servers were becoming synonymous with industry leadership.

Entering 2017, it seemed like all systems were a-go for Liang and team. They enjoyed a strong industry position, they were gobbling market share, they had deep industry ties within Silicon Valley, and the skies were ever blue.

But troubles began bubbling up in 2017, which would become the precursor to far greater issues on the horizon.

Nasdaq Delisting

In 2017, it was revealed that the company was improperly and prematurely recognizing revenue for fiscal 2015 through fiscal 2017.

This came to light in a very innocent way. The company had a shipment stopped at an international border, and that stoppage caused the delivery to leak over into the next fiscal quarter. However, the company had already accounted for the shipment and recognized the revenue in the prior quarter. This small example, while immaterial in isolation, led the company to investigate its reporting practices in more detail.

They found numerous other issues. The 2017 issues highlighted the trouble with Supermicro’s rapid growth and homegrown operations. Their internal ERP systems did not scale with the company’s global presence, and they had issues with reporting. While the reporting itself was never meant to mischaracterize revenue, all the revenue was indeed very real, it highlighted that the company was far behind in internal controls.

As an example: they might buy insurance on cargo, which changes revenue recognition procedures that they didn’t account for. They were accounting for revenue prior to delivery, when the cargo still belonged to them during delivery since it was insured. They should have been recognizing revenue upon delivery, not upon shipment. Their ERP system and accounting procedures were insufficient for their scale. And that needed to change.

While the company was reviewing its internal systems and amending previously misstated revenue figures, they missed a few quarterly reports.

Accordingly, the company was delisted from the Nasdaq in August 2018, in what became a deeply embarrassing event. It took until January 2020 to return to the Nasdaq, after the company upgraded its ERP systems and the SEC signed off on belated financial statements. The company was refreshed, it had cleaned up shop a bit.

What changed?

Perry Hayes, then head of Investor Relations (he left the company in 2020), said: “Internal management’s changed. We have a chief of compliance officer. We didn’t have a senior level auditor reporting to the board: now we do. We had a CFO change; new staff within the management and the accounting group. We also changed our head of sales… In addition to that, we hardwired in some of the internal controls and processes around the revenue recognition to prevent some of those things from happening. Our board of directors has also been changed; we now have three CFOs on the board of directors…”

Liang himself was never accused of misconduct, but had to give back $2.1 million in previously awarded stock-based comp.

After it was said and done, Liang was quoted as saying: “Supermicro is committed to conducting our business ethically and transparently… We fell short of our standards, and we have implemented numerous remedial actions and internal control enhancements to prevent such errors from recurring.”

The 2017 delisting was just the beginning of troubles for Supermicro.

Geopolitical Nightmare: Chinese Spy Chips

With the 2017 delisting still stinging Supermicro and tarnishing their reputation, 2018 would prove to be some of the darkest days of Liang’s life.

What began in 2015 as pre-acquisition due diligence by Amazon would eventually become an uncontrollable geopolitical nightmare for Supermicro.

Bloomberg broke this story in the October 4th, 2018 edition of Businessweek. The story follows as such:

Amazon wanted to acquire Elemental Technologies in 2015 and began proper due diligence on its operations. Elemental Technologies was a leader in video-compression software. Amazon Web Services wanted this technology in their datacenters.

Elemental was founded in 2006 by three engineers that wanted to optimize the time it took to process large video files. GPUs were the leading solution at the time, and Supermicro offered industry-leading GPU server configurations. They were naturally the best choice for Elemental's servers.

In 2009, Elemental began working with In-Q-Tel, the CIA’s investment arm, and this gave their software, built on Supermicro hardware, inroads throughout the US military. As a result, Supermicro began establishing itself as a reliable hardware vendor for the US government and military.

By 2014, the US government began investigating the possibility of spy chips implanted into Elemental hardware.

They kept this quiet and highly classified, in part because they didn’t want China to suspect the investigation, but also because they didn’t want to cripple Supermicro's reputation.

What began as a regular course of due diligence swiftly became a monumental geopolitical event. Amazon's third-party testing found tiny chips implanted into the servers that were not part of the original design specs. Amazon promptly reported these findings to the US government, and it was treated as a severe risk. After all, numerous US government agencies had Supermicro hardware.

In some cases, the chips were implanted between memory and logic dies, giving them the capability of intercepting data in transit on the chip. Amazon and the US government elected to keep this quiet and instead hack the chips to learn more about the origins.

After all, quickly replacing all the hardware would suggest to China that the US knew what was going on. Amazon discovered also that its China-based hardware was comprised. The AWS hardware in China was seen as diseased and was ultimately sold to Beijing Sinnet, a Chinese cloud provider.

In tandem with this, Apple began investigating its hardware and found similar spy chips in 2015. They promptly went nuclear and severed their entire relationship with Supermicro and replaced all the servers.

The US government would then look deeply into Supermicro’s supply chain and finally traced down four main sub-contractors that could have been infiltrated by an arm of the People’s Liberation Army, PLA, that specialized in hardware manipulation. China’s military was bribing or threatening these subcontractors to implant spy chips into Supermicro servers, the end customers of which were US government agencies, major US enterprises like Apple and Meta, and major US financial institutions.

The spy chips alone weren’t big enough to cause major issues. What came next was a vulnerability in Supermicro’s software update process. They used an online portal to process software updates with customers.

In 2015, this portal was breached by China, a breach that was discovered by Facebook. In 2016, Apple reported a similar issue. This would allow China to infiltrate the servers during the firmware update and connect to the spy chips, offering unmitigated access to all customer data running on Supermicro servers.

On October 4th, the day of this report, Supermicro stock tanked 40%. The market panicked.

After all, this was Bloomberg, after all. And Bloomberg had statements as compelling as: "You have to think of Supermicro as the Microsoft of hardware [...]. Attacking Supermicro's motherboards is like attacking Windows. It's attacking the whole world," a former U.S. intelligence official was quoted as saying by Bloomberg BusinessWeek, adding that the group has "more than 900 customers in 100 countries," including the U.S. Department of Defense. As well as Apple and Amazon."

This story marked a grim day for Supermicro and Charles Liang.

Basically all Supermicro hardware was tainted and quickly became the centerpiece of intense geopolitical conflict. They were blindsided.

Or so the story goes.

Everyone involved vehemently denied these allegations brought forth by Bloomberg. What began as an irreversible stain on Supermicro’s legacy quickly became an embarrassment for Bloomberg.

Apple, Amazon, Supermicro, and even the Department of Defense fiercely denied these findings. The DoD even said they were “befuddled” with the findings. Others called into question the reporters’ motives, credentials, and professionalism. Cybersecurity experts pointed out numerous inconsistencies in the story.

Supermicro eventually regarded the report as fake news. The proof is in the pudding - they contracted a third-party tester, and the reports came back positive: no malware. The only major contract they lost was with Apple, all other major customers conducted investigations and decided to stay with Supermicro.

Following the 2018 allegations, and exacerbated by the pandemic supply chain issues, Supermicro moved all of their principal manufacturing operations out of China and into Taiwan, Malaysia, the Netherlands, and San Jose.

What could have been the end of this company was quickly left in the rear-view. Wall Street has all but forgotten these allegations, as Supermicro jumped aboard the AI hype train and its stock has been on an unstoppable rocket ship journey upwards.

All Aboard! The AI Hype Train Departs

In 2020, they were first to market with AMD EPYC processors. In 2021, they announced over 100 application specific product SKUs.

On September 20th, 2022, Supermicro announced their H100 optimized server portfolio. They beat all other server OEMs except Dell, who made the announcement the same day. Entering 2023, Supermicro began experiencing strong momentum driven by optimistic sentiment. The late November 2022 launch of ChatGPT would herald in a wave of intense demand for AI accelerated hardware.

On January 31st, 2023, Supermicro reported 53% YoY revenue growth in Fiscal Q2, 2023. Alongside this was a gross margin expansion from 14% to 18.7% and YoY earnings growth of 319% ($42m to $176m). On March 21st, 2023, Supermicro announced their 8-H100 Nvidia GPU servers. On March 22nd, they announced deskside liquid-cooled AI platforms that include a 3-year subscription to Nvidia AI enterprise and ultimately won NAB Show product of the year for the AI category.

On May 2nd, 2023, they reported a slowdown in sales both QoQ and YoY but reported YoY growth in earnings. Despite the slowdown, the market rewarded Supermicro's narrative of strong AI demand:

"Supermicro continues to see record levels of engagements in our new generation product lines, especially for AI applications," said Charles Liang, President and CEO of Supermicro. "We secured several new and large design wins and are deploying some of the world’s most leading GPU clusters. With the recent new key components supply chain challenges mostly in the rear-view mirror and production normalizing, we expect to gain share and expand scale as we emerge as the true leader for rack-scale Total IT Solutions"

On May 22nd, they announced the industry's first rack-scale GPU based liquid cooled system, a first mover advantage that will benefit them as we enter the Blackwell era.

The stock reached a 2023 high around $350 prior to their fiscal Q4 earnings report despite strong sales and earnings growth. The company noted weakness in GPU supply and revised down guidance, leading to a months long sideways trading range.

In November 2023, they announced manufacturing capacity reached 5k racks per month and support for the Nvidia H200 superchip. In December 2023 the stock was punished by an equity offering.

Supermicro's fate would change in a major way on January 18th when they pre-released earnings showing a major beat on previous guidance driven by strong AI demand:

This sent the stock rocketing from $311 to $495 on the January 29th earnings call. On January 29th, the company reported sales and earnings that beat the January 18th guide.

By February 15th, the stock had run to $1,004 marking a 258% YTD price appreciation.

On Friday, March 1st 2024 the stock ran another 20%, eclipsing the $1,000 threshold yet again. This was driven by the announcement that they would be included in the S&P in the March 15th, 2024 rebalancing.

That brings us to today. The stock currently trades around $1,030 and hit as high as $1,155 so far this year. S&P inclusion should bring with it immense institutional inflows, but many in the market are skeptical that this mania is sustainable.

One thing is for certain, though. This company was not reactive to the AI demand boom, their positioning was simply a product of their business model and first-to-market strategy.

Regardless of future stock price performance, this company benefits universally from advancements in the semiconductor industry. They provide solutions for datacenter AI, edge AI, telecom enhancements, and numerous other computing segments.

Management noted in the January earnings call that they are now working on the shift from Supermicro 3.0 (Total IT Solutions) to Supermicro 4.0. What this will be is unknown, but the market will certainly be paying closer attention to this company moving forward.

The major question now is, when will demand dry up?

That's when the rocket ship comes back to earth.